We have entered an era where

artworks are traded like securities. With the institutionalization of the “Art

investment contract security,” fractional investment platforms are entering the

formal financial sphere. Companies like YeolMae Company and Artipio are leading

this movement, promoting a new fusion of art and finance. For investors, it

presents a new concept called “Art-Tech,” and for issuers, it suggests

opportunities for diversifying revenue models and expanding the market.

However, the market response has

fallen far short of expectations. Low subscription rates and increasing

self-underwriting by issuers indicate that the market has yet to build

meaningful trust. Most crucially, it raises the fundamental question: Do the

artworks underlying these securities actually meet the basic standards of

investable assets?

The First Doubts About Work

Suitability

In early 2025, Artipio issued its

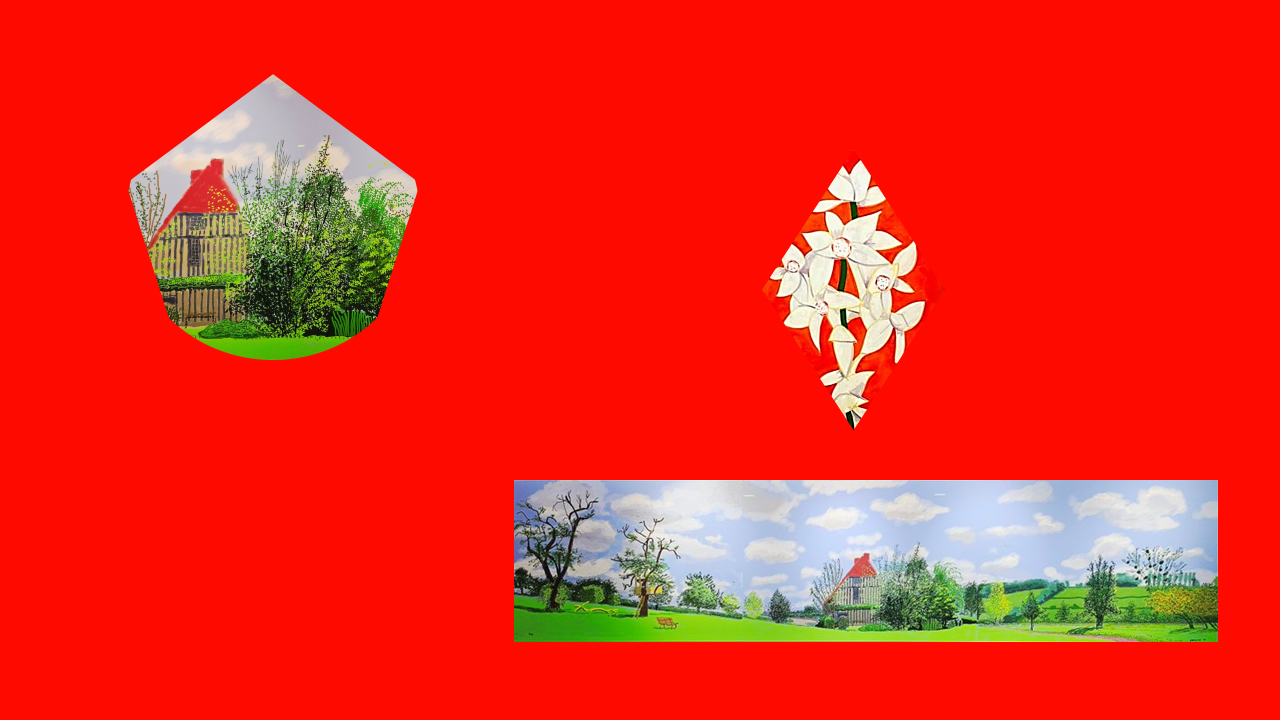

first art investment contract security based on David Hockney’s iPad drawing,〈30th May 2021, From the Studio〉.

While Hockney is undoubtedly a globally recognized name, this particular work

was Edition No.11 out of 25 — a digital print with limited rarity or

uniqueness. The digital format itself further weakens its liquidity and

long-term value in the secondary market.

Artipio’s First Underlying Asset: David Hockney, 〈30th May 2021, From the Studio〉, 65.5 cm × 282 cm, edition 11 of 25./ Photo: Artipio

Despite these clear limitations,

Artipio purchased the work for hundreds of millions of KRW and issued it as a

financial product — a move that appears to have prioritized name recognition

over artistic or intrinsic value. This decision highlights a troubling tendency

to favor superficial recognizability over curatorial discernment when

determining what constitutes a bankable artwork.

A Structural Lack of Curatorial

Competence

The same problem emerged in

Artipio’s second offering. This time, the underlying asset was Alex Katz’s〈Cymbidium Yellow on Red〉, a painting that deviates from his most iconic style

and lacks significant market visibility. It has low liquidity and limited

transaction records, making it a questionable candidate for securitization.

Predictably, investor demand was poor, and the issuer was forced to absorb most

of the offering itself.

Alex Katz’s 〈Cymbidium Yellow on Red〉, the underlying asset for Artipio’s second art investment contract security / Courtesy of Artipio

This repeated pattern points to

more than a marketing failure — it exposes a deep structural flaw: the absence

of curatorial expertise within the securitization framework. Selecting artworks

for financial products requires analysis of the artist’s place in art history,

collector demand, gallery representation, and market comparables. Currently,

such comprehensive evaluation appears absent from the selection process for

these securities.

The Problem of Missing Experts

Firms like YeolMae Company and

Artipio claim to conduct their own valuation and selection processes, but few

verifiable details exist about the experts involved.

YeolMae has promoted its proprietary algorithm for art valuation, but the

methodology remains undisclosed. Since artworks are not traded on real-time

exchanges and have inherently unstable pricing, valuations rely heavily on

qualitative factors — comparable sales, artist trajectories, and market

narratives. This makes the role of trained art experts absolutely critical.

Inadequate valuation processes undermine the credibility of public disclosures

and erode investor trust.

Market Reactions and Structural

Limits

As of mid-2025, both of Artipio’s

investment securities have recorded disappointing subscription rates. The first

Hockney-based product reached only 39.3%, while the second Katz-based one fell

further to just 13.3%. In both cases, the issuer had to underwrite the majority

of the offering, signaling that the products failed to function as true public

offerings.

YeolMae Company faces similar

challenges. Its 2024 revenue fell by 33% year-over-year, and delays in new

securities offerings have forced it to rapidly pivot toward NFTs and art-backed

loans. These moves reflect a deeper reality: the art securities market is not

yet institutionally, regulatorily, or commercially ready to succeed.

The Danger of Financial Experiments

Without Artistic Insight

Attempts to financialize art are

not new, but successful cases remain few and far between. Artistic value cannot

be reduced to fame or surface-level attributes. Context, historical

significance, collector interest, and expert validation all matter.

Yet the current crop of art investment securities in Korea largely sidesteps

these elements, focusing instead on external packaging and speculative promise.

This not only destabilizes the market but also undermines investor confidence.

What the Market Needs is Not

Technology, But Discernment

Turning art into financial products

requires far more than technical tools or structural innovation. It demands

deep knowledge of art and a nuanced understanding of the market. Without the

eye of the curator, robust data on the art economy, or the ability to interpret

the cultural narrative around artists and works, no financial product can be

sustainable — let alone credible.

Artipio’s decision to offer a

high-priced digital edition drawing by David Hockney as its flagship investment

product reveals the stark absence of artistic judgment in the market.

Products created by people who cannot recognize artistic value are doomed to

fail. The real crisis in the art securities market today is not a lack of

innovation, but a lack of competence, responsibility, and vision among those

leading it.